Editor: Noopur Date

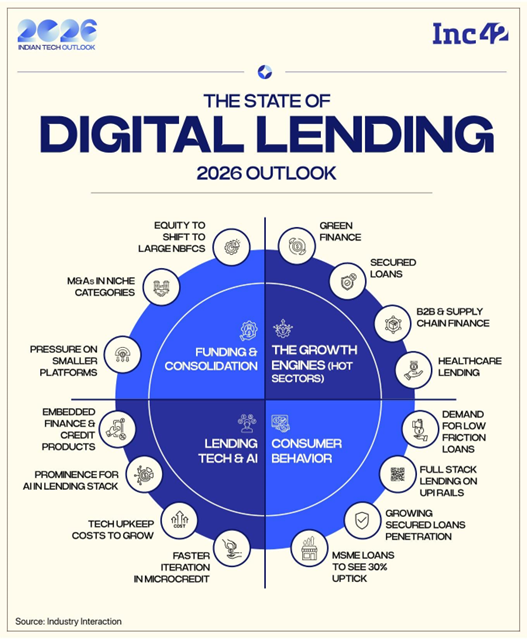

India’s credit landscape is undergoing a profound transformation as digital technologies reshape the way loans are originated, underwritten, and delivered. Over the past decade, fintech platforms, non-banking financial companies (NBFCs), and digital ecosystems have enabled borrowers to access credit instantly through smartphones. The scale of this transformation is remarkable. Digital lending is projected to become a $1.3 trillion market opportunity in India by 2030, growing nearly fivefold from around $270 billion in 2022.

India’s Credit Evolution Growth Story

Evolving from a bank-dominated lending system to a technology-enabled digital credit ecosystem, India’s credit market has undergone a significant transformation. The evolution of India’s credit market accelerated with the expansion of retail lending in the 2000s and 2010s. The turning point came with the development of India’s digital public infrastructure, including Aadhaar-based digital identity, e-KYC systems, and real-time payment platforms. These innovations drastically reduced the cost of customer verification and transaction processing, allowing financial institutions to digitize large parts of the lending process.

Digital lending platforms emerged as key players in this new ecosystem by combining technology-driven underwriting with efficient distribution channels. By 2030, lending technology is expected to contribute more than 53% of fintech revenues, making it the dominant segment of the industry. According to industry estimates, India’s digital lending market is projected to grow fivefold as fintech adoption increases.

Source: Inc42

Business Model of Digital Lending Firms

The business model of digital lending in India revolves around using technology platforms to originate, assess, and distribute loans more efficiently than traditional banking channels.

- In some cases, fintech companies function as balance sheet lenders, where licensed NBFCs directly provide loans from their own capital and earn revenue through interest income, processing fees, and penalties.

- However, a large part of the industry follows a platform or marketplace model, where fintech firms act as intermediaries connecting borrowers with regulated lenders such as banks or NBFCs.

- A common structure is the co-lending model, in which fintech companies collaborate with banks to jointly fund loans and share risks and returns.

- Some of the modern business models include embedded finance and Buy Now Pay Later (BNPL) services, where credit is integrated directly into e-commerce platforms, payment apps, or merchant ecosystems, allowing consumers and small businesses to access credit at the point of transaction.

Economic Benefits

Specifically, digital lending has enabled millions of first-time borrowers to access formal credit. According to recent lending reports, India’s retail loan portfolio has continued to grow steadily, with overall retail loans increasing by 18.1% year-on-year as of late 2025, reflecting strong demand for consumer and business credit. Beyond individual borrowers, credit is becoming more accessible to micro-entrepreneurs, gig workers, and small merchants in rural markets. However, the rapid pace of credit expansion raises the risk of borrower over-leveraging.

Downside of Digital Lending in India

A significant portion of digital loans consists of small-ticket unsecured personal loans, which typically carry higher default risks than secured credit. If underwriting standards weaken or borrowers accumulate excessive debt, this could create vulnerabilities within the financial system. Concerns have also emerged regarding certain lending applications that engage in predatory practices, including excessive fees, aggressive recovery methods, and misuse of personal data. The ratio for unsecured retail loans increased from 1.56% in March 2024 to 1.82% in March 2025.

Regulatory Scenario

The Reserve Bank of India (RBI) has repeatedly cautioned that rapid growth in fintech-driven lending. The Digital Lending Directions (September 2022, updated on 2025) issued by the central bank establish guidelines to improve transparency, borrower protection, and data privacy. Beyond lending-specific reforms, regulators are also strengthening the broader digital financial ecosystem.

Moreover, Recent initiatives include tighter rules on fraud protection and authentication mechanisms for digital transactions, reflecting the growing importance of security in India’s expanding digital finance landscape. Overall, these regulatory reforms signal a shift toward “innovation with safeguards.”, while policymakers continue to support fintech-driven credit expansion.

Future of Digital Lending in India

Ultimately, the future of India’s digital lending sector will depend on its ability to balance innovation with risk management. If fintech companies successfully combine advanced data analytics, embedded financial services, and responsible lending practices, digital credit could become a powerful driver of financial inclusion and economic growth.

However, the sector’s rapid expansion also presents challenges, particularly as more than 70% of fintech loan portfolios consist of unsecured credit, raising concerns about potential credit risk and borrower over-indebtedness. In summary, the digital lending sector is expected to grow at ~30% CAGR between 2024–2030. The industry is likely to witness greater consolidation and stronger regulatory alignment.

{kind=link}

Leave a comment