Editor: Khushi Koolwal

Over the last decade, finance has undergone multiple waves of digital transformation like mobile banking, UPI, algorithmic underwriting, and AI-powered risk analytics. But the next transformation will be far more fundamental: the tokenization of real-world assets (RWAs). This process, where physical or traditional financial assets are represented as digital tokens on a blockchain, has the potential to reshape capital markets, democratize access to investment opportunities, and unlock trillions of dollars in global liquidity.

Global financial institutions such as Black Rock, Vanguard, JP Morgan, HSBC, and regulators like the Monetary Authority of Singapore (MAS) are already piloting tokenization. As the technology matures, the question is no longer whether RWA tokenization will transform finance, but how fast and to what extent.

What is RWA Tokenization?

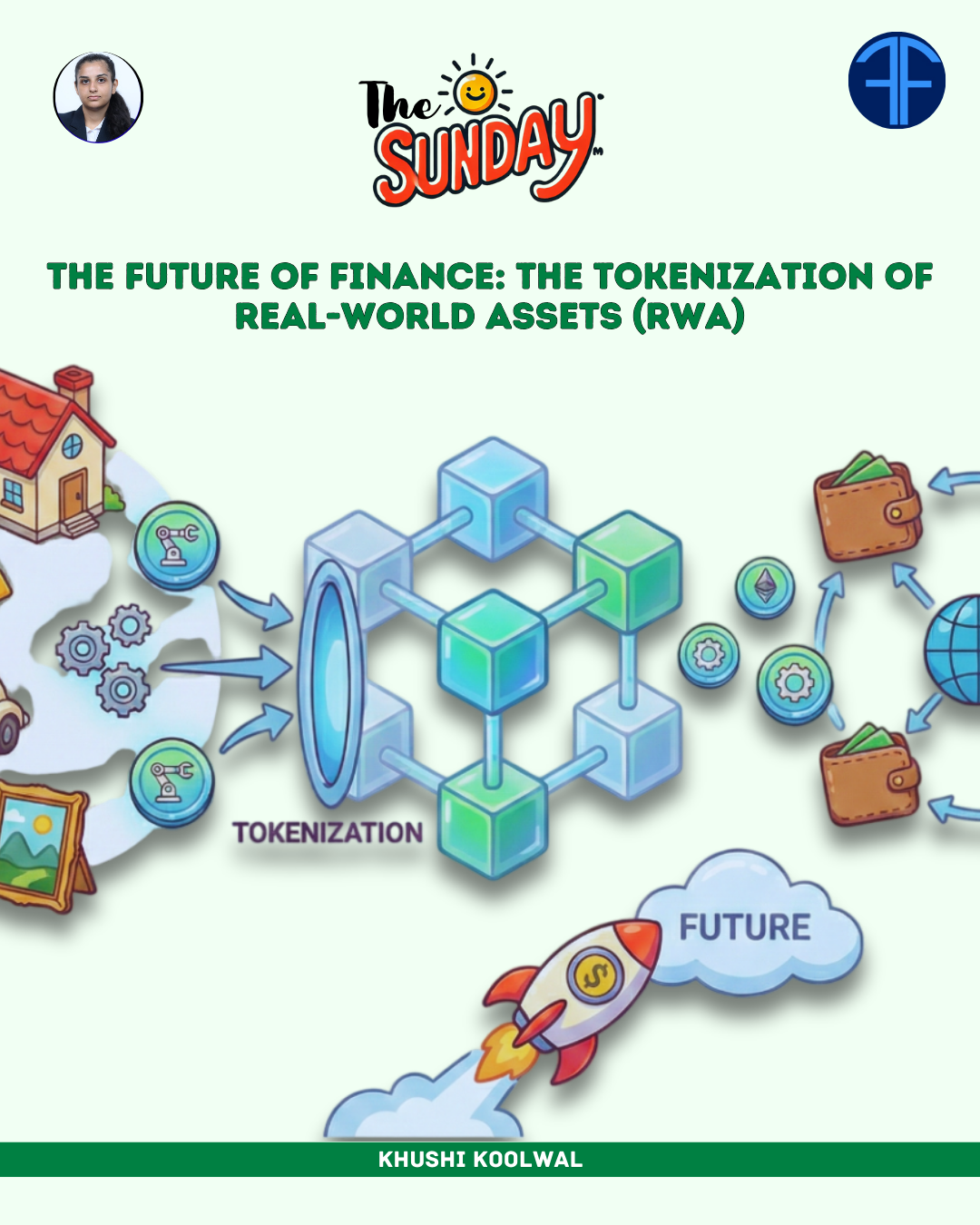

RWA tokenization is the process of converting the ownership rights of tangible and intangible assets into digital tokens on a blockchain. This movement is not just about creating digital collectibles; it is a fundamental re-engineering of the global finance, leading to much greater liquidity and widespread access to investments.

For example, a commercial property worth ₹50 crore can be represented as millions of digital tokens, allowing investors to buy even a tiny fraction. Each token reflects verifiable ownership and can be traded instantly. This simple shift turns assets that were historically illiquid or accessible only to wealthy investors into instruments that can be traded globally and more efficiently.

Why Tokenization is Gaining Momentum

Tokenization is gaining traction due to a powerful mix of institutional adoption, technological maturity, and investor demand. Large institutions such as JP Morgan and Black Rock are leading institutions that lend credibility to the space. Regulators across Singapore, the UK, and Europe are creating sandboxes to safely test tokenized financial products, signalling a shift from scepticism to structured experimentation.

Meanwhile, blockchain technology has become more scalable and secure and global investors are increasingly seeking liquidity solutions beyond traditional markets. These trends collectively push tokenization from a theoretical possibility into an emerging financial reality.

Use Cases Across Finance

The most prominent application of tokenization today is in bonds and treasuries, where settlement can be completed within minutes instead of days, significantly reducing operational and counterparty risks. Real estate is another important use case, as tokenization enables fractional ownership, automated rent distribution, and global participation in property markets.

Private credit and supply-chain finance, particularly relevant to emerging markets like India, can benefit from improved transparency, easier credit scoring, and reduced fraud. Even commodities like gold and luxury assets such as art or collectible watches are being tokenized to provide liquidity and open access to broader investor groups.

Challenges: The Gap Between Promise and Reality

Even though tokenization sounds very promising however there are some real problems that need to be solved.

First, the rules are not clearin many countries. Governments haven’t fully decided how tokenized assets should be treated are they like shares, documents, or something new? Because of this, companies are scared to use them widely.

Another issue is safety of the real asset. If a property or gold is tokenized, someone still needs to physically store and protect that asset. If the company managing it is not trustworthy, investors may lose their money. There are also technology risks. Smart contracts (the computer code used in tokenization) can have mistakes or can be hacked, which may lead to financial loss.

Different blockchains also have trouble communicating with each other, so tokens created on one system may not work smoothly on another. This makes trading difficult. And finally, just creating tokens is not enough. There must be buyers and sellers in the market. If very few people are using tokenized assets, then trading will remain slow and the benefits will not be fully realized.

So, for tokenization to grow properly, we need clear rules, safe systems, trustworthy managers, better technology, and more people using it.

The Road Ahead

In the future, tokenization will likely become a normal part of how the finance world works. Today, our financial system uses many middlemen and takes time to settle transactions. But with blockchain, everything can become faster, cheaper and more secure. Financial markets may also work 24 hours a day, 7 days a week, just like crypto markets do now. This means people can buy or sell assets anytime, not only during bank hours.

It is not just about bringing existing assets to the blockchain, it’s about creating entirely new financial products that are programmable, composable and instantly liquid. As regulatory clarity emerges and institutional-grade infrastructure is built, the RWA market is poised for explosive growth. The tokenization of everything is a slow, methodical revolution, but its impact is certain. By breaking down the barriers of scale and time that have defined finance for centuries, RWA tokenization is building a more accessible, efficient, and truly global financial ecosystem

{kind=link}

Leave a comment